TL;DR:

- The Enterprise Investment Scheme (EIS) is a UK government initiative offering up to 30% income tax relief on investments in early-stage companies to stimulate growth funding. It also provides capital gains tax exemption, loss relief, and CGT deferral protections, making it highly tax-efficient and risk-mitigated. The scheme is extended until 2035, with strict eligibility and compliance requirements for both companies and investors.

The Enterprise Investment Scheme (EIS) is a UK government-backed tax incentive that gives investors up to 30% income tax relief on qualifying investments in early-stage companies. Administered by HMRC, the scheme is one of the most generous tax-efficient investment structures available in the UK. For startups seeking growth capital and for individuals looking to reduce their tax liability, understanding what the enterprise investment scheme means is the first step toward using it effectively. This article covers the definition, tax reliefs, eligibility criteria, the claiming process, and the 2026 updates you need to know.

What does enterprise investment scheme mean and how does it work?

The Enterprise Investment Scheme is a UK government venture capital tax incentive designed to channel private capital into qualifying small companies. HMRC oversees the scheme, and it sits alongside the Seed Enterprise Investment Scheme (SEIS) and Venture Capital Trusts (VCTs) as part of the government’s broader toolkit for stimulating early-stage investment. The core mechanism is straightforward: an investor puts money into a qualifying company, holds the shares for at least three years, and in return receives a package of tax reliefs that significantly reduce the financial risk of the investment.

The scheme targets early-stage companies planning long-term growth, and legislative changes introduced in 2014, 2015, and 2018 tightened compliance rules to exclude tax-motivated investments with limited genuine risk. This is not a loophole. It is a deliberate policy tool designed to direct capital toward businesses that would otherwise struggle to attract funding. For founders, that means EIS is both an investor attraction tool and a compliance obligation.

What tax reliefs and benefits does the enterprise investment scheme offer?

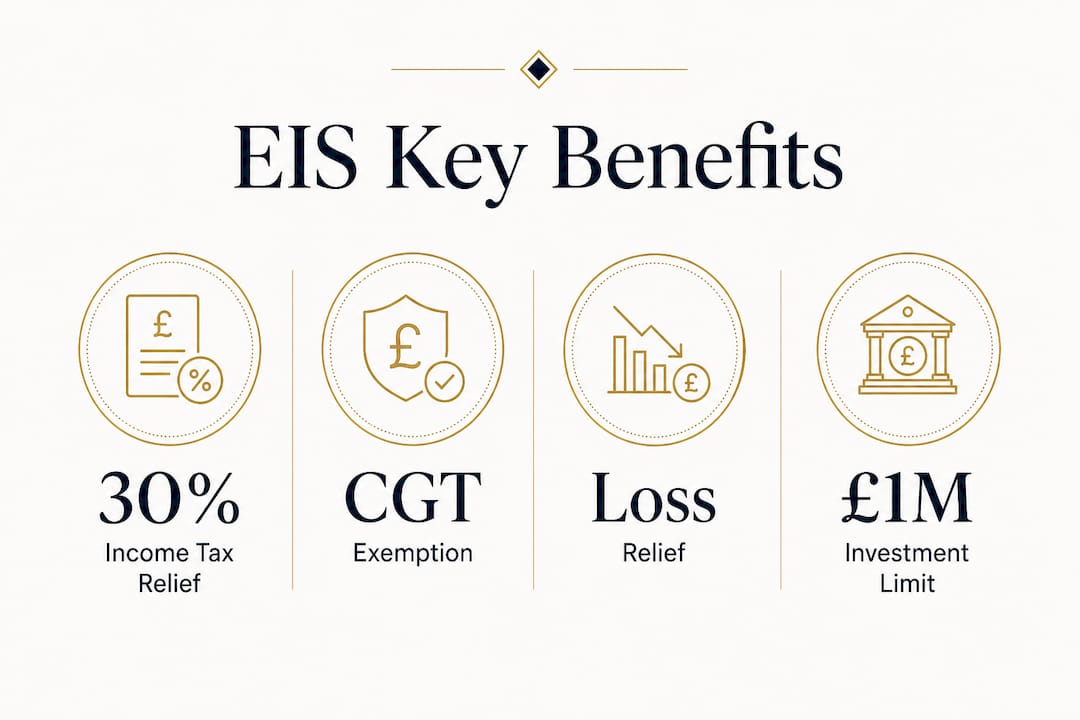

EIS income tax relief is 30% on the amount invested, with a maximum of £1 million per tax year. That means an investor committing £100,000 to an EIS-qualifying company can reduce their income tax bill by £30,000 in the year of investment. For investors putting money into knowledge-intensive companies (KICs), the annual limit doubles to £2 million, provided at least £1 million of that total is invested in KICs. This higher ceiling makes KIC-qualifying startups particularly attractive to high-net-worth investors.

Beyond income tax relief, EIS offers three additional protections that reduce investment risk considerably:

- Capital gains tax (CGT) exemption. Gains on EIS shares held for at least three years are free from CGT entirely, provided income tax relief was claimed and not withdrawn.

- Loss relief. If an EIS investment fails, investors can offset the net loss against their income tax or capital gains tax liability, reducing the effective downside.

- CGT deferral. Investors can defer a capital gain from another asset by reinvesting it into EIS shares. The gain is deferred until the EIS shares are sold.

The combination of these reliefs means the effective risk on an EIS investment is substantially lower than on an unprotected equity stake. A basic-rate taxpayer investing £10,000 into a qualifying company receives £3,000 back in income tax relief immediately, and if the company fails entirely, loss relief reduces the net loss further.

Pro Tip: Investors must hold a valid EIS3 or EIS5 certificate to claim any relief. Without these documents, HMRC will not process the claim, regardless of how long shares have been held.

| Relief type | How it works |

|---|---|

| Income tax relief | 30% of investment deducted from income tax bill, up to £1m (£2m for KICs) |

| CGT exemption | No capital gains tax on profits from EIS shares held three or more years |

| Loss relief | Net losses offset against income tax or CGT if the investment fails |

| CGT deferral | Capital gains from other assets deferred by reinvesting into EIS shares |

Which companies and investors qualify for the enterprise investment scheme?

EIS eligibility criteria apply to both the company receiving investment and the individual investing. Companies must meet all of the following conditions at the time of investment:

- Maximum of 249 full-time equivalent employees (499 for knowledge-intensive companies)

- Gross assets of no more than £30 million before the investment is made

- Annual fundraising limit of £10 million under EIS (£20 million for KICs)

- The company must be unquoted and not controlled by another company

- Trading must be in a qualifying activity. Excluded trades include property development, financial services, legal and accountancy services, and farming

Knowledge-intensive company status is granted to companies that meet specific criteria around research and development expenditure or the proportion of skilled employees engaged in innovation. This status unlocks the higher investment limits described above and makes a company significantly more attractive to larger investors. Founders in life sciences, deep tech, and advanced manufacturing should assess KIC eligibility early in their fundraising planning.

On the investor side, the rules are less complex but still carry conditions. You cannot claim EIS relief on shares in a company where you are already a director at the time of investment, unless you become a director after the investment is made. You also cannot be a connected person, meaning you cannot hold more than 30% of the company’s shares or voting rights. The minimum holding period for retaining relief is three years from the date of share issue or the commencement of trading, whichever is later.

The risk to capital condition introduced in 2018 is the most significant compliance test. It requires that the investment carries genuine risk of capital loss and that the company intends to grow and develop over the long term. Arrangements designed primarily to generate tax relief with minimal commercial risk will fail this test and disqualify the investment entirely.

How does the enterprise investment scheme process work for raising funds?

The practical process for using EIS has several distinct stages, and missing any one of them can block investors from claiming relief.

- Apply for advance assurance. Before launching a fundraising round, most companies apply to HMRC for advance assurance. This is not mandatory, but it confirms that the company and the proposed share issue are likely to qualify. Investors frequently require advance assurance before committing funds.

- Issue shares and submit compliance statement. After shares are issued, the company submits a compliance statement (form EIS1) to HMRC. This triggers HMRC’s review of whether the company and the investment meet all qualifying conditions.

- Receive EIS3 certificates. Once HMRC approves the compliance statement, it issues EIS3 certificates to the company, which then distributes them to investors. For investments made through an approved EIS fund, investors receive an EIS5 certificate instead.

- Claim relief on Self Assessment. Investors use the information on their EIS3 or EIS5 certificate to complete their Self Assessment tax return and claim income tax relief.

- Maintain qualifying conditions for three years. Both the company and the investor must continue to meet EIS conditions throughout the three-year holding period. Any breach, such as a change in trading activity or a share disposal, can trigger clawback of relief already claimed.

Pro Tip: Founders should prepare EIS paperwork before opening a funding round, not after. Delays in issuing EIS3 certificates frustrate investors and can push claims into the wrong tax year, reducing the scheme’s appeal.

The most common pitfall is a company failing to issue EIS3 certificates promptly after HMRC approval. Without valid certificates, investors cannot claim any relief, which undermines the entire rationale for investing through EIS in the first place. Good record-keeping and a clear internal process for certificate issuance are not optional.

What are the key updates and nuances affecting EIS in 2026?

The most significant recent development is the legislative extension of EIS and VCT schemes. In the Autumn Statement 2023 and Budget 2024, the government confirmed that both schemes would continue until 2035, extending the previous 2025 sunset clause by a decade. This gives investors and companies a long planning horizon and removes the uncertainty that had begun to dampen EIS activity in the years leading up to 2025.

HMRC data shows that in 2024 to 2025, 3,735 companies raised £1,575 million under EIS. This figure confirms that the scheme remains a significant source of early-stage capital in the UK, channelling over £1.5 billion into qualifying businesses in a single tax year.

“EIS is not merely an investment incentive but a policy tool to direct capital to early-stage UK businesses with growth potential, emphasising compliance and risk to capital.”

The narrowing of eligible activities over successive legislative changes means that fewer companies qualify today than a decade ago. Businesses in excluded sectors such as property, finance, and professional services cannot use EIS regardless of their size. For those that do qualify, the knowledge-intensive company designation is increasingly worth pursuing, as it unlocks the higher £2 million investor limit and signals credibility to sophisticated investors.

| Factor | Standard EIS | Knowledge-intensive company |

|---|---|---|

| Max employees | 249 | 499 |

| Max gross assets | £30 million | £30 million |

| Annual fundraising cap | £10 million | £20 million |

| Investor annual limit | £1 million | £2 million |

Key takeaways

The Enterprise Investment Scheme delivers 30% income tax relief, CGT exemption, and loss relief to investors in qualifying UK companies, making it one of the most tax-efficient investment structures available to individuals and startups.

| Point | Details |

|---|---|

| Core definition | EIS is a HMRC-administered tax incentive offering 30% income tax relief on qualifying investments. |

| Certificate requirement | Investors must hold a valid EIS3 or EIS5 certificate before any relief can be claimed. |

| Eligibility conditions | Companies must have fewer than 250 employees, gross assets under £30m, and trade in qualifying activities. |

| KIC advantage | Knowledge-intensive companies unlock a £2m investor limit and a £20m annual fundraising cap. |

| Legislative certainty | EIS is confirmed to run until 2035, giving investors and founders a stable long-term planning window. |

Why EIS planning should start before the pitch deck

From my experience working with founders and investors across the UK, the single most common mistake with EIS is treating it as an afterthought. Companies launch funding rounds, secure commitments, and only then discover that their trading activity partially falls into an excluded category, or that their corporate structure fails the risk to capital test. By that point, the investor has already made a decision based on the assumption of EIS relief. Unwinding that expectation is damaging.

The founders who use EIS most effectively are those who treat qualification as a structural design question from day one. They review the founder legacy planning checklist before incorporating, they apply for advance assurance before opening a round, and they build certificate issuance into their post-investment process as a formal obligation, not an administrative footnote.

EIS is also frequently misunderstood as purely an investor benefit. It is equally a founder tool. A company that can credibly offer 30% income tax relief, CGT exemption, and loss relief to investors is raising capital in a fundamentally different conversation than one that cannot. The scheme reduces investor hesitation and broadens the pool of individuals willing to back early-stage risk. Used properly, it is one of the most powerful fundraising assets a qualifying UK company has.

— Blackbook

Protect your investment structure with Blackbookprotocol

Understanding EIS is one part of the picture. Structuring your investment, corporate governance, and asset protection correctly is the other.

Blackbookprotocol provides expert blueprints for UK trust law, equity structuring, and tax-efficient asset protection. Whether you are a founder preparing for an EIS funding round or an investor building a tax-efficient portfolio, the Blackbook Protocol hardback gives you the governance frameworks and compliance tools to protect what you build. For founders who want to align EIS planning with broader trust law compliance, the protocol covers both in detail. Download the protocol and secure your financial structure today.

FAQ

What does enterprise investment scheme mean in simple terms?

The Enterprise Investment Scheme is a UK government programme that gives investors income tax relief of 30% when they invest in qualifying small companies. It is administered by HMRC and designed to encourage private capital into early-stage businesses.

How much tax relief can I claim through EIS?

Investors can claim 30% income tax relief on up to £1 million invested per tax year, or up to £2 million if at least £1 million is invested in knowledge-intensive companies. Relief is claimed through Self Assessment using an EIS3 or EIS5 certificate.

What are the EIS eligibility criteria for companies?

Qualifying companies must have fewer than 250 employees, gross assets under £30 million, and raise no more than £10 million per year under EIS. They must also trade in a qualifying activity and pass the risk to capital condition introduced in 2018.

How long must I hold EIS shares to keep the tax relief?

Investors must hold EIS shares for a minimum of three years from the date of issue or the start of trading, whichever is later. Disposing of shares before this period triggers clawback of income tax relief already claimed.

Is EIS still available after 2025?

Yes. The government confirmed in the Autumn Statement 2023 and Budget 2024 that EIS and VCT schemes are extended to 2035, providing a decade of legislative certainty for both investors and qualifying companies.

0 Kommentare