TL;DR:

- Gifts where the donor retains benefits are considered gifts with reservation, which remain part of the estate for inheritance tax purposes. These rules apply regardless of the paperwork, including living rent-free in a gifted property or continuing income from gifted assets. Proper documentation and early risk assessments are essential to avoid significant tax liabilities upon death.

Many people assume that giving away an asset removes it from their estate for inheritance tax purposes. That assumption is wrong when a gift with reservation is involved. Under UK law, if you give away an asset but continue to benefit from it, HMRC treats it as though you never gave it away at all. The legal and tax implications of a reservation gift can be severe, and they catch out even well-intentioned estate planners. This guide explains exactly how these rules work, what they mean for your estate, and how to avoid costly mistakes.

Table of Contents

- Key takeaways

- What is a gift with reservation under UK law?

- Examples of gifts with reservation in practice

- Conditional gifts versus gifts with reservation

- Inheritance tax implications and planning steps

- Cross-jurisdictional perspectives on gift taxation

- My perspective on gifts with reservation

- Protect your estate with the Blackbook Protocol

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Legal definition matters | A gift with reservation means gifting an asset whilst retaining a benefit from it, triggering specific UK tax rules. |

| Inheritance tax exposure | Gifted assets where benefit is retained are included in your estate for inheritance tax at death, despite the earlier transfer. |

| Distinct from conditional gifts | Gifts with reservation differ fundamentally from conditional gifts, which attach conditions rather than ongoing donor benefit. |

| HMRC anti-avoidance intent | The rules exist specifically to prevent inheritance tax avoidance through paperwork transfers that change nothing in practice. |

| Planning can prevent problems | Identifying and addressing reservation issues early, with professional advice, avoids unintended tax liabilities. |

What is a gift with reservation under UK law?

A gift with reservation of benefit is a specific legal and tax concept under UK law. It arises when a person gives away an asset but continues to receive some form of benefit from it after the transfer. The Finance Act 1986 s 102 and its related subsections form the statutory basis for these rules, giving HMRC the power to re-include gifted assets in a deceased person’s estate for inheritance tax purposes.

The core principle is straightforward. If you give something away on paper but nothing changes in practice, the law does not treat the gift as complete. Gift with reservation rules assess tax consequences based on true benefit retention rather than legal paperwork alone. This is the anti-avoidance logic at the heart of the legislation.

It is worth distinguishing this concept from a conditional gift in contract law or estate planning. A conditional gift attaches conditions to the transfer itself, such as a requirement that the recipient reaches a certain age. A gift with reservation, by contrast, focuses on what the donor continues to enjoy after the gift has been made. The distinction matters enormously for tax.

Key features of the gift with reservation rules include:

- The donor must have made a genuine gift of the asset.

- The donor must continue to benefit from the asset after the transfer.

- The benefit must be more than merely incidental or trivial.

- HMRC applies these rules regardless of the donor’s intention.

Pro Tip: If you are unsure whether a benefit you retain from a gifted asset crosses the legal threshold, seek specialist tax advice before assuming the gift is clean. The cost of getting it wrong is measured in inheritance tax at 40%.

Examples of gifts with reservation in practice

The most widely cited example is also the most common. You transfer your home to your children but continue to live in it without paying a market rent. Gifting a home but living rent-free is the classic trigger for gift with reservation rules, and the property remains part of your taxable estate at death as though the transfer never happened.

But property is not the only asset that creates problems. Consider these further scenarios:

- Family business shares. You gift shares in a family company to your children but continue to receive dividends from those shares. The retained income stream constitutes a benefit, and the gift may be treated as a reservation.

- Investments and savings. You transfer a portfolio to a trust but retain the right to draw income from it. The ongoing income benefit brings the assets back into scope.

- Chattels and personal property. You give away valuable artwork or jewellery but keep it displayed in your home. Continued use and enjoyment can constitute a reservation.

- Agricultural or commercial land. You transfer farmland to a family member but continue to farm it without paying a commercial rent. The farming activity itself may represent a retained benefit.

The practical impact on inheritance tax assessment is significant. GWR rules re-characterise gifts for tax purposes to prevent avoidance by retaining benefits after gifting, treating the asset as still owned by the donor at the date of death. This means the full market value at death is included in the estate, not the value at the date of transfer. In a rising property market, this distinction alone can represent hundreds of thousands of pounds of additional tax exposure.

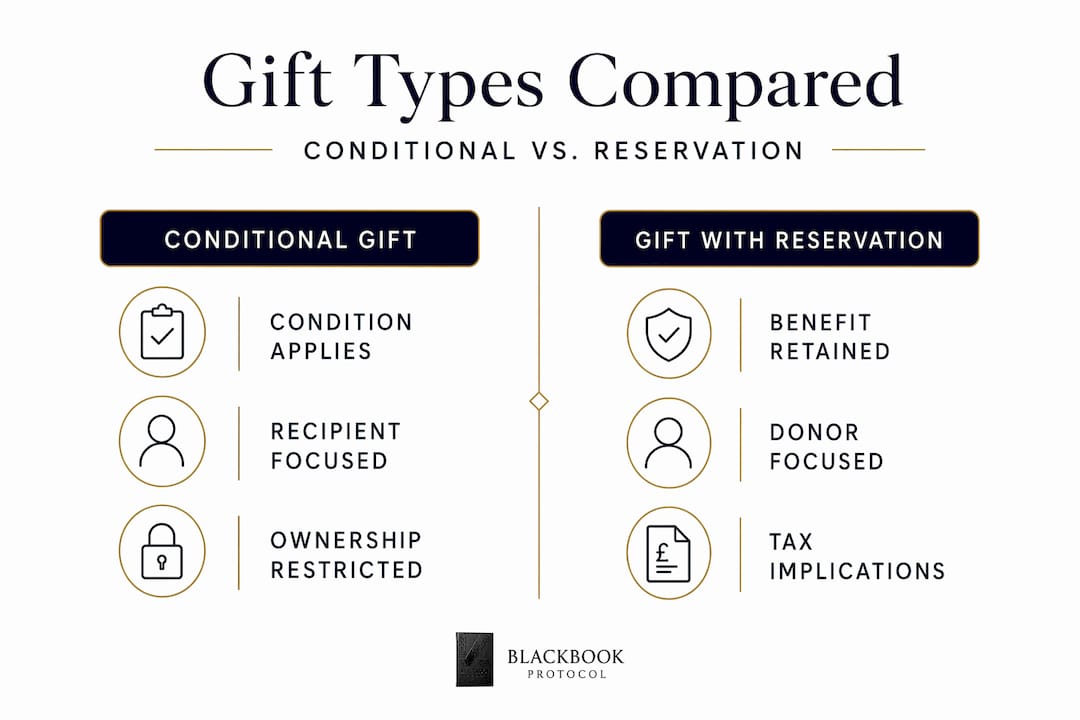

Conditional gifts versus gifts with reservation

These two concepts are frequently confused, and the confusion carries real tax risk. Understanding the difference between a conditional gift and a gift with reservation is not merely academic.

A conditional gift in estate planning involves a condition attached to the transfer itself. Conditional gifts involve conditions precedent or subsequent that govern whether or when the recipient’s ownership becomes absolute. A condition precedent must be satisfied before the gift takes effect. A condition subsequent can defeat the gift after it has been made. Neither of these involves the donor retaining a personal benefit.

A gift with stipulations, by contrast, is not really about conditions on the recipient at all. It is about what the donor continues to enjoy.

| Feature | Conditional gift | Gift with reservation |

|---|---|---|

| Focus | Conditions on the recipient | Benefit retained by the donor |

| Tax treatment | Generally outside the estate if complete | Treated as part of the estate for IHT |

| Legal basis | Contract and trust law | Finance Act 1986 s 102 |

| Revocability | Depends on the condition type | Not revocable, but benefit retention is the issue |

| Planning risk | Lower if properly structured | High if benefit is not clearly severed |

The question of whether a gift can be revoked is also relevant here. A gift with reservation is not technically revocable by the donor, but the reservation itself means the gift has not achieved its intended tax purpose. Ceasing the benefit entirely, for example by moving out of the gifted property and paying a full market rent, can release the reservation going forward. However, the period during which the reservation applied will still carry tax consequences.

Pro Tip: When drafting any gift with stipulations, document clearly what benefit, if any, the donor retains. Ambiguity is what HMRC exploits when assessing whether a reservation exists.

Inheritance tax implications and planning steps

The inheritance tax consequences of a gift with reservation are the primary reason this area demands careful attention. Continuing rent-free occupation triggers gift with reservation rules, causing the asset to be taxed in the estate as though no gift was ever made. At a 40% inheritance tax rate above the nil-rate band, the financial cost of an unintentional reservation can be substantial.

HMRC’s position is clear: the legal implications of a reservation gift are assessed on substance, not form. A transfer that changes nothing in practice changes nothing for tax.

Here are the key steps to identify and manage gift with reservation risks in your estate plan:

- Audit all previous gifts. Review every asset transfer made in the past seven years and assess whether any benefit was retained after the transfer date.

- Assess current benefit retention. For any asset you have gifted, ask honestly whether you still derive any use, income, or advantage from it.

- Obtain a market valuation. If a reservation exists, understand the current market value of the asset, since this is the figure that will be included in your estate at death.

- Consider releasing the reservation. If possible, cease the benefit entirely or begin paying a full market rent. Document the change formally and date it precisely.

- Review trust structures. Trusts can be affected by reservation rules if the settlor retains any benefit. Review trust deeds with a specialist to confirm the position.

- Update your will and estate plan. Ensure your will reflects the actual composition of your estate, including any assets that may be pulled back in by reservation rules.

- Seek specialist tax advice. The rules have nuances and exceptions. A qualified tax adviser or solicitor should review your position before you assume a gift is effective for inheritance tax purposes. Reviewing common estate planning mistakes can also help identify where reservation issues typically arise.

One important exception: if you gift your home and then move out permanently, paying a full market rent to the new owner, the reservation can be released. The asset will no longer be included in your estate from the point the reservation ceases, though the period of reservation still counts.

Cross-jurisdictional perspectives on gift taxation

UK gift with reservation rules are specific to UK inheritance tax legislation, but it is useful to understand how other jurisdictions approach similar issues, particularly if you hold assets abroad or have family members in other countries.

In the United States, the gift tax system operates differently:

- The US applies a gift tax on the donor, not the recipient, with an annual exclusion of $19,000 for 2025 and 2026.

- Donors of future interest gifts must file Form 709 gift tax returns by 15 April of the year following the gift.

- The US does not have a direct equivalent of the UK gift with reservation concept, though retained interests in trusts can trigger inclusion rules under different provisions.

- US estate and gift tax rules interact with a lifetime exemption that is substantially higher than the UK nil-rate band.

The terminology also differs. What the UK calls a gift with reservation of benefit, the US might address through grantor trust rules or retained interest provisions. If you hold assets in multiple jurisdictions or are considering cross-border transfers, the interaction between these systems can create unexpected double-tax exposure. Professional advice from advisers qualified in both jurisdictions is not optional in those circumstances. Understanding how to divide inherited property across borders adds further complexity that warrants specialist input.

My perspective on gifts with reservation

I have seen more estate plans undermined by gift with reservation issues than by almost any other single mistake. The pattern is consistent. A parent gifts their home to their children, assumes the job is done, and nobody revisits the arrangement for a decade. By the time the estate is administered, the asset has appreciated significantly, and the inheritance tax bill reflects a value the family never anticipated.

What I have learned is that the problem is rarely malicious. People genuinely do not understand that benefit retention defeats the tax purpose of a gift. The paperwork looks complete. The legal title has moved. But HMRC looks at substance, and substance is what matters.

The other thing I would stress is documentation. If you have made a gift and you want to argue that no reservation exists, you need contemporaneous evidence. A letter confirming the terms, a formal tenancy agreement at market rent, board minutes if a company is involved. Verbal arrangements and family understandings do not hold up under scrutiny.

My advice is always the same. Do not assume. Review every gift you have made, assess whether any benefit remains, and get a qualified opinion on the tax position before the estate is administered. Proactive planning costs a fraction of what reactive damage limitation costs.

— Blackbook

Protect your estate with the Blackbook Protocol

Understanding gift with reservation rules is the foundation. Building a structure that actually protects your estate requires going further.

The Blackbook Protocol is a practical, expert-authored guide to UK trust law, asset protection, and tax-efficient estate governance. It covers the structures that work, the mistakes that cost families their legacies, and the specific mechanisms, including 95/5 equity splits and trust frameworks, that give you genuine control over how your assets are held and transferred. Whether you prefer the hardback edition or the Kindle version, the protocol gives you a blueprint that goes well beyond general awareness into applied strategy. If you are serious about securing your legacy, this is where to start.

FAQ

What is a gift with reservation of benefit?

A gift with reservation of benefit is a gift where the donor continues to benefit from the asset after transferring it. Under Finance Act 1986 s 102, HMRC includes such assets in the donor’s estate for inheritance tax at death.

How does a gift with reservation work for inheritance tax?

The gifted asset is treated as though it was never given away. Its full market value at the date of death is included in the taxable estate, potentially triggering a 40% inheritance tax charge above the nil-rate band.

Can a gift be revoked once made?

A gift with reservation is not revocable by the donor. However, the donor can release the reservation by ceasing to benefit from the asset, for example by moving out of a gifted property and paying a full market rent, which removes the asset from the estate going forward.

What are examples of conditional gifts versus gifts with reservation?

A conditional gift attaches conditions to the recipient’s ownership, such as reaching a certain age. A gift with reservation involves the donor retaining personal benefit after the transfer, such as living in a gifted home rent-free. These are legally and tax distinct concepts.

Does paying rent on a gifted property remove the reservation?

Yes, if the donor pays a full market rent to the new owner, the reservation is released from that point. The asset will no longer be included in the estate for inheritance tax, though any period of prior reservation still carries tax consequences.

Recommended

- Blackbook Protocol Hardback | Asset Protection & Corporate Governance – BLACKBOOK PROTOCOL

- BLACKBOOK PROTOCOL Kindle eBook | Asset Protection & Corporate Governance

- Blackbook Protocol | UK Trust Law & Asset Protection Guide 2026 – BLACKBOOK PROTOCOL

- Blackbook Protocol | UK Trust & Asset Protection Guide – BLACKBOOK PROTOCOL

0 comments