TL;DR:

- Portfolio segregation involves legally separating client assets from those of the firm to prevent commingling and protect investments during insolvency. Regulatory rules, such as SEC Rule 15c3-3, enforce operational controls and daily reconciliations to ensure proper asset isolation and safeguard investor holdings. It differs fundamentally from diversification, which reduces market risk but does not provide legal asset protection in case of a firm’s failure.

Portfolio segregation is one of those financial concepts most people assume they understand until they actually need to rely on it. Knowing what does portfolio segregation mean goes beyond a textbook definition. It determines whether your assets survive a broker’s insolvency, whether a fund structure legally protects one class of investors from another’s losses, and whether the safeguards you believe are in place actually hold up in a dispute. This article covers the definition, legal structures, regulatory enforcement, and practical application of portfolio segregation for individuals and finance professionals alike.

Table of Contents

- Key takeaways

- What does portfolio segregation mean?

- Legal structures that enable segregation

- Regulatory and operational enforcement

- Segregation vs pooled funds and diversification

- How to apply portfolio segregation in practice

- My take on what segregation actually delivers

- Protect your assets with Blackbook Protocol

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Segregation is legal isolation | Portfolio segregation separates client assets from firm assets by law, not merely by intent or account labelling. |

| SPCs ring-fence at entity level | Segregated portfolio companies create legally distinct sub-portfolios within one entity, isolating liabilities between investors. |

| Regulation drives compliance | SEC Rule 15c3-3 and similar rules mandate reserve accounts, custody controls, and daily reconciliations to prove segregation. |

| SMAs offer direct ownership | Separately managed accounts give investors legal title to underlying securities, unlike pooled funds where you own a share of a collective pot. |

| Segregation is not diversification | Buying multiple assets reduces risk but provides no legal isolation. True segregation requires structural and operational separation. |

What does portfolio segregation mean?

At its core, portfolio segregation means keeping client investments and cash entirely separate from the assets of the broker, fund manager, or financial firm holding them. The purpose is to prevent commingling. If a broker faces insolvency, a properly segregated client account cannot be drawn into the firm’s general pool of assets to settle creditors. Your holdings remain yours.

This is not a voluntary best practice. It is a regulatory requirement in most major financial jurisdictions, and it carries real legal teeth.

A few distinct concepts sit under the portfolio segregation umbrella:

- Segregation of client assets from firm assets. The broker or manager holds your securities and cash in accounts kept entirely apart from the firm’s own capital.

- Segregated portfolio companies (SPCs). A single legal entity divided into legally distinct sub-portfolios, each with its own assets and liabilities that cannot be touched by creditors of another sub-portfolio.

- Separately managed accounts (SMAs). An individual account in which the investor holds direct legal ownership of the underlying securities, separate from any pooled structure.

Portfolio segregation is frequently confused with diversification. Diversification is a portfolio construction strategy. It reduces market risk by spreading holdings across asset classes, sectors, or geographies. Segregation, by contrast, is a legal and operational mechanism. You can hold a single concentrated position in a fully segregated account, or you can hold a highly diversified mutual fund in which you have no legal isolation from other investors whatsoever. The concepts address completely different problems.

Legal structures that enable segregation

Segregated portfolio companies

A segregated portfolio company is a single legal entity divided into separate portfolios, each of which has its own assets and liabilities ring-fenced by statute. BVI law is a well-established jurisdiction for these structures, offering a framework where each portfolio operates as though it were a standalone entity for liability purposes. If portfolio A suffers losses or faces claims, the assets of portfolio B are protected. Creditors of one sub-portfolio have no recourse to another.

This structure is increasingly used for specialist investment funds, captive insurance arrangements, and multi-class investment vehicles where investor isolation is a primary requirement. Properly administered SPCs limit liability contamination between portfolios, but this protection depends entirely on accurate allocation of assets and liabilities at the entity level.

Separately managed accounts

SMAs provide direct ownership of the underlying securities, which means the investor holds legal title to each stock, bond, or other instrument in the account. This is categorically different from buying units in a mutual fund, where your legal claim is to a proportionate share of a collective pool.

The practical significance is considerable. In an insolvency scenario, an SMA investor can assert direct ownership over specific securities. A mutual fund investor becomes an unsecured creditor of the fund structure, which is a materially weaker position.

| Feature | Separately managed account | Pooled fund |

|---|---|---|

| Legal ownership | Direct title to securities | Proportionate claim on pool |

| Transparency | Full visibility of holdings | Periodic aggregate disclosure |

| Insolvency protection | Stronger direct recourse | Creditor claim on pooled assets |

| Customisation | Tailored mandates possible | Standardised fund strategy |

| Minimum investment | Typically higher | Lower entry point |

Pro Tip: When evaluating a segregated structure, ask your custodian or administrator for written confirmation of the legal basis for segregation, not merely a reference to account names or fund documentation. The legal basis must be statutory or trust-based, not just contractual.

Regulatory and operational enforcement

Regulation is what transforms intent into reality in portfolio segregation. Rules exist precisely because voluntary commitment to segregation is insufficient when firms face financial pressure.

-

SEC Rule 15c3-3 is the primary US regulation governing broker-dealer custody of client assets. It requires broker-dealers to hold fully paid client securities separately and maintain a special reserve account formula to ensure sufficient liquid assets are available to meet client claims at all times. Recent amendments require daily reserve computations for certain broker-dealers, tightening the operational burden and reducing gaps where commingling could occur.

-

Custodian activity segregation extends beyond securities holding. SEBI’s 2026 circular requires custodians to maintain clear operational separation between their regulated and unregulated service lines, with distinct accounts for each. This prevents client assets held in one service category from being exposed to liabilities generated by another.

-

Reconciliation and recordkeeping are the operational backbone of any segregation arrangement. Segregation audits focus heavily on the reconciliation of securities and cash, ensuring client assets can be clearly identified and are not mixed with firm resources. Account names and policy statements are not sufficient. Auditors require documented controls, regular reconciliations, and evidence that procedures are actually followed.

-

Reserve formulas and custody controls under regulatory enforcement rely on mathematical formulas and defined custodial obligations, not stated intentions in client agreements. This is a critical point. A firm can have a contractual obligation to segregate and still fail to do so operationally. The regulatory framework exists to make operational failure costly and detectable.

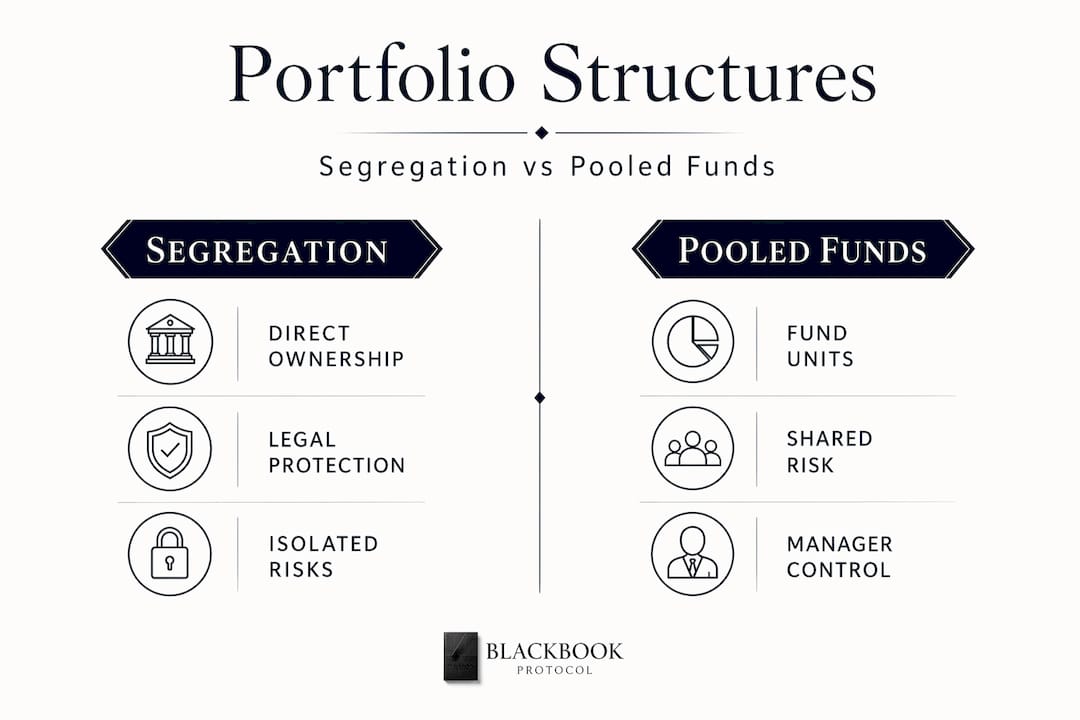

Segregation vs pooled funds and diversification

The importance of portfolio segregation becomes clearest when you compare it directly to the alternatives most investors actually use.

Pooled funds and the ownership gap

When you invest in a standard mutual fund, you do not own the securities inside it. You own units in the fund. The fund owns the securities. Investors have direct legal ownership in SMAs but only claims on pooled holdings in mutual funds, which affects asset protection materially in an insolvency scenario.

The gap matters less when markets are functioning normally. It becomes critical when a fund manager faces regulatory action, fraud allegations, or insolvency. In those situations, your ability to recover assets depends on the legal structure, not the stated intentions of the fund documentation.

The diversification confusion

Segregation differs from diversification in a fundamental way. Diversification reduces the probability that all your investments fall in value simultaneously. It does not create any legal barrier between your assets and a third party’s liabilities. You can own a perfectly diversified portfolio inside a non-segregated structure and still lose everything if the custodian or manager fails.

Consider the comparison:

- A diversified portfolio held in a pooled fund provides risk reduction against market volatility but no protection against the fund’s operational failure.

- A concentrated single-stock holding in a properly segregated SMA provides no market risk reduction but full legal isolation from the custodian’s insolvency.

These are different tools. Using one does not substitute for the other.

| Concept | Risk addressed | Legal protection | Mechanism |

|---|---|---|---|

| Diversification | Market and concentration risk | None | Asset allocation across holdings |

| Portfolio segregation | Counterparty and insolvency risk | Yes, by law | Legal and operational separation |

| Pooled fund | Market risk | Limited | Collective ownership structure |

How to apply portfolio segregation in practice

Knowing the theory is useful. Knowing what to actually check when structuring or evaluating an arrangement is more useful still.

When you assess a segregated account or fund structure, the following points warrant close examination. The benefits of portfolio segregation include enhanced asset protection, reduced risk exposure, and clearer accountability, but only if the structure is correctly set up and administered.

First, confirm the legal basis. Is segregation achieved through statute, trust law, or contract? Statutory and trust-based segregation are materially stronger than purely contractual arrangements. A holding company structure in a suitable jurisdiction may provide additional layers of separation for complex asset arrangements.

Second, assess the custodian. Who holds the assets? Are they regulated? Do they maintain segregated sub-accounts, or do they operate an omnibus account where your holdings are pooled with others? Investor control over underlying assets through a segregated account allows tailored risk management and tax optimisation that pooled structures cannot offer.

Third, review the administration. Statutory protection in an SPC only functions if the entity is properly administered with precise allocation and recordkeeping. Ask for evidence of reconciliation procedures, audit trails, and how assets are allocated between sub-portfolios if applicable.

Fourth, understand what happens in default. If the manager, broker, or custodian fails, what is the recovery process? Is there a statutory framework, a compensation scheme, or solely a contractual claim? If asset seizure by a regulatory body is a concern, understanding how creditor claims interact with segregated structures is worth examining before a problem arises, not after.

Pro Tip: Most investors never ask for the specific custody agreement between their fund manager and the custodian. This document defines the actual segregation mechanism. Requesting it is entirely reasonable and reveals more about the real protection in place than any fund factsheet.

My take on what segregation actually delivers

I’ve reviewed enough fund structures and investor complaints to form a fairly direct opinion on this. Portfolio segregation is genuinely protective when it is properly constructed and administered. It is almost useless when it exists only on paper.

The most common failure I’ve seen is not fraud or deliberate commingling. It is administrative sloppiness. An SPC structure with two active sub-portfolios and inconsistent allocation records is legally vulnerable. A segregated account with a custodian who runs omnibus books and reconciles quarterly rather than daily is not delivering what the client believes it is delivering.

The other thing worth saying directly: segregation is often sold as a premium feature, a marker of sophistication. In practice, the value it provides depends entirely on the jurisdiction, the administrator’s rigour, and the specific legal basis of the arrangement. I’d prioritise those three factors over any branding or marketing language attached to the word “segregated.”

Regulatory environments are tightening. The SEC’s move to daily reserve computations and SEBI’s 2026 activity segregation circular both point in the same direction. Regulators are less willing to accept procedural segregation that isn’t backed by daily operational evidence. For investors, this is a positive development. For firms that have been managing segregation loosely, it represents a material compliance burden.

— Blackbook

Protect your assets with Blackbook Protocol

Portfolio segregation is one piece of a larger asset protection framework. Understanding the legal mechanics of segregation puts you ahead of most investors. Putting those mechanics into a coherent structure that includes trust law, equity arrangements, and tax-efficient governance is where the real work begins.

Blackbookprotocol has produced a detailed resource for individuals and finance professionals who want to move from understanding to implementation. The Blackbook Protocol hardback covers UK trust law, corporate governance, and asset protection structures in a format designed for practical use, not shelf display. If you prefer digital access, the Kindle edition covers the same ground with the same level of depth. Both are built around the same principle: structure your assets correctly before you need the protection, not after.

FAQ

What does portfolio segregation mean in simple terms?

Portfolio segregation means keeping a client’s assets legally and operationally separate from those of the firm or other investors managing or holding them. It prevents commingling and protects client assets if the firm fails.

How does portfolio segregation differ from diversification?

Diversification spreads investment risk across multiple assets. Portfolio segregation creates legal isolation between your assets and a third party’s liabilities. One is a portfolio construction technique; the other is a legal protection mechanism.

What is a segregated portfolio company?

A segregated portfolio company is a single legal entity divided into distinct sub-portfolios, each with its own ring-fenced assets and liabilities. Creditors of one sub-portfolio cannot make claims against the assets of another.

What is an SMA and how does it relate to portfolio segregation?

A separately managed account gives an investor direct legal ownership of the underlying securities in their portfolio. This provides stronger legal protection than pooled funds, where investors hold only a proportionate claim on a collective pool.

How is portfolio segregation enforced in practice?

Regulators such as the SEC require broker-dealers to maintain reserve accounts, hold client securities separately, and conduct regular reconciliations. Operational proof of segregation, not just contractual intent, is required to satisfy compliance obligations.

0 commenti