TL;DR:

- Owning shares does not equate to controlling a company; governance structures determine actual decision-making power.

- Founders risk losing control over time due to dilution, funding provisions, and board shifts unless deliberate protective measures are negotiated early.

Most founders assume that owning shares means owning control. That assumption costs them their companies. What does control retention mean for founders? It means preserving your authority to make strategic decisions, set company direction, and determine your own future as the organisation grows. Not just your percentage of the cap table. Founder control is fundamentally a governance issue, and the gap between economic ownership and actual decision-making power widens dramatically with every funding round you close.

Table of Contents

- Key takeaways

- What control retention means for founders

- How control erodes through funding rounds

- Legal mechanisms to preserve founder control

- Operational control: delegation and leadership

- The long-term impact of control retention

- My perspective on control retention

- How Blackbookprotocol supports founders on control

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Equity is not control | Owning shares does not guarantee voting power or board influence; governance structure determines actual control. |

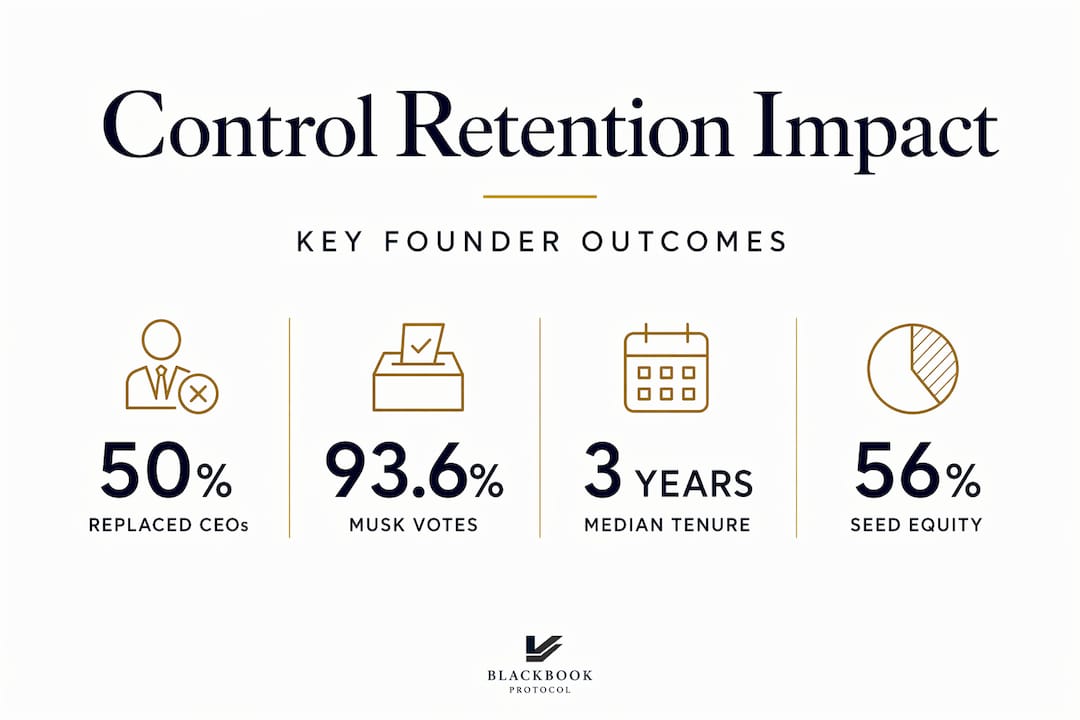

| Dilution follows a predictable path | Founders typically hold 56% at seed and just 16.1% at Series C, losing governance leverage at each stage. |

| Legal tools exist to protect control | Dual-class shares, board composition rights, and protective provisions can preserve founder authority through dilution. |

| Delegation is a form of control | Retaining operational influence requires structured delegation, not micromanagement or total abdication. |

| Early negotiation is decisive | Provisions negotiated at seed set the governance pattern for every subsequent round; vague terms compound over time. |

What control retention means for founders

Control retention, at its most precise, refers to a founder’s ongoing ability to direct company strategy, governance, and key decisions. It is not simply a control retention definition tied to share percentage. Two founders can each own 20% of their company and have completely different levels of actual authority, depending on the governance instruments in place.

The distinction matters most between economic ownership and voting power. Economic ownership determines how much of the financial upside you receive. Voting power determines whether you can approve a new investor, block a sale, or remove a board member. These two things can diverge sharply as soon as you issue preferred shares.

Key structural elements that define control retention in practice:

- Voting rights attached to share classes. Ordinary shares may carry one vote each; preference shares may carry none, or they may carry specific veto rights on defined decisions.

- Board composition. Who appoints directors, and how many seats does each party control? A founder with 40% equity but the right to appoint three of five board members holds more practical control than one with 60% equity and no board appointment rights.

- Protective provisions. Preferred shareholders hold veto rights on specific decisions, independently of any board vote. These can include approval over new share issuances, acquisitions, or changes to the articles of association.

- Dual-class share structures. Class B shares commonly carry ten votes per share compared to one vote for Class A. This allows founders to retain majority voting power even as their equity percentage falls.

Elon Musk’s structure at SpaceX illustrates this precisely. Through 93.6% super-voting Class B shares, he retains majority voting control post-IPO despite holding a minority economic stake. Most founders do not negotiate structures this extreme, but the principle applies at every stage.

Pro Tip: Do not treat the term sheet as the final word on governance. The certificate of incorporation and shareholder agreement contain the binding provisions. Read both before signing anything.

How control erodes through funding rounds

Control erosion follows a predictable pattern. Understanding it is the first step toward countering it. Founders typically hold 56% equity at seed, dropping to 36% at Series A, and further to 16.1% at Series C. At that point, governance leverage at the board table has often already transferred to investors.

| Funding stage | Median founder equity | Governance risk level |

|---|---|---|

| Seed | 56% | Low |

| Series A | 36% | Moderate |

| Series B | ~25% | High |

| Series C | 16.1% | Critical |

The equity decline itself is only part of the picture. Several structural instruments accelerate the loss of control beyond what the raw percentages suggest:

- Liquidation preferences. Investors with 1x, 2x, or participating preferred terms receive their capital back first in any exit. This reduces the founder’s effective leverage in sale negotiations.

- Anti-dilution ratchets. Weighted average or full ratchet provisions adjust investor share counts upward when a down round occurs. This further dilutes founders without any new capital entering the company.

- Board composition shifts. As rounds progress, investors typically gain the right to appoint independent directors or board observers. With an even number of directors and no casting vote, founders can find themselves outvoted on decisions they built the company to make.

“Investors prioritise economic returns over long-term company health, marginalising founders through governance rather than equity.”

The human cost of this erosion is significant. 50% of startup founders are replaced as CEO within three years, and only 40% remain by year four. Founder removal frequently occurs not because the business is failing, but because governance provisions negotiated early have shifted control to investors who prefer a different operator.

Legal mechanisms to preserve founder control

Founder control retention is achievable, but it requires deliberate structuring from the earliest stage. Governance structures and contract details are the primary instruments founders use to maintain strategic authority. The table below compares the most commonly used mechanisms:

| Mechanism | How it works | Best for |

|---|---|---|

| Dual-class shares | Class B shares carry 10x votes | Founders who expect high dilution |

| Odd-numbered board | Prevents deadlock; founder holds casting vote | Early-stage governance control |

| Protective provisions | Require founder consent on defined decisions | Blocking adverse investor actions |

| Acceleration clauses | Vest remaining equity on exit or role removal | Protecting founder economics on departure |

| Drag-along rights | Define conditions under which sale can proceed | Preventing forced exits at low valuations |

The most durable approach is dual-class share structures. Class B shares with multiple votes held by founders preserve voting control despite equity dilution. Google, Meta, and Snap all use this structure. For UK-incorporated companies, similar results can be achieved through weighted voting rights in the articles of association, though the mechanism is structured differently than US equivalents.

Board composition is equally consequential. An odd number of directors is standard practice for a reason. It prevents deadlock. Where the founder holds a casting vote as chairperson, governance control is preserved even when the equity picture has shifted substantially. You should also consider your founder legacy planning position at each funding milestone, not just at exit.

Equity structuring must be treated as a living process, adapting governance rights across rounds rather than accepting standard investor templates wholesale.

Pro Tip: Negotiate your board composition rights and voting provisions at seed. These terms set the pattern for every subsequent round. Vague provisions in the first shareholders’ agreement will be cited against you in every document that follows.

Operational control: delegation and leadership

Legal ownership and governance rights create the conditions for control. What you do with those conditions is a leadership question. Many founders conflate retaining control with doing everything themselves. That conflation is where operational control breaks down.

Effective delegation is not the same as outsourcing execution to people you do not trust. Delegation requires clear briefs, defined trust levels, and structured feedback loops. Without those three elements, the founder remains an execution bottleneck regardless of how good the team is.

The transition from maker to leader is one of the hardest identity shifts in business. Many first-time founders are afraid to delegate, which produces a version of control that is actually anxiety: the founder remains involved in every decision because no system exists to handle decisions without them.

Here is a practical framework for operational control retention:

- Define the decision clearly. Before delegating anything, specify what decision is being made, what authority the delegate holds, and what requires escalation.

- State the output, not the method. Control the outcome you need, not the process used to reach it. This frees your team to operate without constant check-ins.

- Set a review cadence. Agree in advance when and how you will review outcomes. This creates a feedback loop without constant interference.

- Distinguish reversible from irreversible decisions. Reversible decisions can be delegated with minimal oversight. Irreversible ones require your direct involvement, regardless of team confidence.

Founders who build these systems retain operational influence across a growing organisation. Those who do not end up either controlling nothing or controlling everything, and neither position scales.

The long-term impact of control retention

The impact of control retention extends well beyond individual decisions. Founder control enables a longer-term discovery process in company growth. When founders lose governance authority prematurely, the organisation shifts toward short-term investor milestones rather than the kind of sustained experimentation that produces category-defining companies.

The trade-off between capital and control is real. External funding accelerates growth but redistributes authority. Founders who understand this trade-off can negotiate it deliberately. Those who do not tend to discover it after the fact, when the provisions are already locked in.

Control retention also affects company culture. A founder who remains in genuine strategic authority sets the values, hiring bar, and product direction of the organisation. When that continuity breaks, culture tends to drift toward whatever the incoming leadership team prioritises, which may not align with what made the company compelling in the first place.

“The ability to retain discovery is the primary reason founder-controlled companies disproportionately produce large outcomes.”

For founders building with long-term intent, the importance of control retention is not abstract. It determines whether you are building your company or someone else’s version of it.

My perspective on control retention

I have worked with enough founders to see a clear pattern. The ones who lose control rarely lose it in a single dramatic moment. They lose it gradually, through provisions they did not fully read, board seats they agreed to in exchange for a better valuation, and governance rights they assumed were standard when they were anything but.

In my experience, the biggest mistake founders make is treating governance as a legal formality. They focus on the headline valuation and leave the structural provisions to the lawyers, who are often working from investor-friendly templates. By the time the terms matter, they are already locked in.

What I have found actually protects founders is specificity at the point of negotiation. Not vague language about “founder consultation” or “reasonable consent,” but precise terms: exactly which decisions require founder approval, exactly how board seats are allocated, exactly what triggers an acceleration clause. Vague provisions provide almost no lasting protection.

The founders who retain meaningful control into Series B and beyond are not the ones who raised at the best valuations. They are the ones who treated every governance document as a long-term contract, because it is.

— Blackbook

How Blackbookprotocol supports founders on control

Building a company with long-term strategic control requires more than a good lawyer and a standard term sheet. Blackbookprotocol provides structured blueprints for founders who want to retain governance authority through funding stages, protect equity through legally sound instruments, and build a company structure that reflects their long-term intent rather than a default investor template.

If you are raising capital or approaching a new funding round, the governance decisions you make now will determine your authority at the board table for years. Blackbookprotocol’s resources on founder equity structuring and UK-specific legal instruments give you a working framework before you sit down to negotiate. The protocol is designed for founders who understand that control is not given. It is structured.

FAQ

What does control retention mean for founders?

Control retention means a founder’s ability to maintain strategic decision-making authority over their company. It covers voting rights, board composition, and governance provisions, not just share ownership percentage.

How does equity dilution affect founder control?

As founders accept investment across funding rounds, their equity percentage falls. Median founder equity drops from 56% at seed to 16.1% at Series C, which typically reduces their leverage at the board table unless specific governance protections are in place.

What is a dual-class share structure?

A dual-class share structure creates two categories of shares with different voting rights. Founders hold Class B shares with multiple votes per share, allowing them to retain majority voting control even after significant equity dilution.

When should founders negotiate control retention provisions?

Founders should negotiate board rights, voting provisions, and protective clauses at the seed stage. These terms establish the governance template for every subsequent round, and weak early provisions are difficult to correct later.

Can founders retain control after bringing in investors?

Yes, provided the right governance instruments are in place. Dual-class shares, carefully structured board composition, and clearly defined protective provisions allow founders to retain meaningful strategic authority through multiple funding rounds.

0 comentarios